What is a Savings Passbook? Conditions, Benefits, and How to Differentiate

Tiết kiệm

30/12/2024

Learn what a savings book is, the requirements to open one, its benefits, and how to distinguish it. Discover a safe financial solution with attractive interest rates at VPBank today!

A savings passbook has long been a safe financial solution for those looking to accumulate wealth and ensure the security of their funds. But do you truly understand what a savings passbook is, its benefits, and how to easily open one at a bank? Below, VPBank will share detailed information to provide you with a comprehensive overview.

1. What is a Savings Passbook?

A savings passbook is a form of bank deposit where a customer places a fixed amount of money into a savings account for a specified period and earns interest as agreed. It's a secure financial accumulation method, suitable for those who want to manage their money effectively and ensure stable funds.

An overview of the basic features of a savings book.

Savings passbooks are generally divided into two main types:

-

Term Savings Passbook: Offers higher interest rates but requires the money to be held for a specific duration (usually from 1 month upwards).

-

Non-Term Savings Passbook: Allows flexible withdrawals at any time, but typically offers lower interest rates.

With a savings passbook, you not only preserve your assets but also generate stable returns thanks to the interest paid by the bank periodically. This is an ideal choice for accumulating money for future goals such as buying a house, studying abroad, or retirement.

2. Differentiating Types of Savings Passbooks

Currently, there are several types of savings passbooks available for you to choose from:

2.1. Based on Deposit Method

When it comes to deposit methods, there are two different types of passbooks:

-

Physical Savings at the Bank (In-Branch): This is the traditional method where depositors visit the bank's counter directly to open a savings passbook. This method suits those who prefer peace of mind and direct interaction with bank staff.

-

Online Savings: With the advancement of technology, many banks now allow customers to deposit savings online through banking apps or websites. Online savings offer convenience and save time as customers can open a savings passbook anytime, anywhere, without needing to visit a physical branch.

Two ways to open a bank savings account.

2.2. Based on Deposit Term

Based on the deposit term, you have two choices:

-

Term Savings Passbook: This type of savings passbook requires customers to deposit money for a predetermined period, such as 1 month, 3 months, 6 months, or 1 year. This type of passbook usually offers higher and fixed interest rates throughout the term. However, if money is withdrawn before maturity, customers will only earn a lower, non-term interest rate as per bank regulations.

-

Non-Term Savings Passbook: With this type of passbook, customers can withdraw money at any time without waiting until maturity. However, the interest rate for non-term savings passbooks is generally lower than for term savings passbooks. This is suitable for those who need high flexibility and can easily access their funds when needed.

3. Benefits of Opening a Savings Passbook

A savings passbook is an ideal and secure financial solution that helps you build a solid financial future. It's a smart investment with many outstanding advantages:

-

Easy Accumulation, Long-term Returns: A savings passbook helps you gradually accumulate assets according to a clear plan. Simply set a goal, choose a suitable term, and consistently deposit money; your balance will grow steadily, meeting all your future needs.

-

Safe Returns, High Efficiency: With attractive interest rates and absolute safety backed by deposit insurance, a savings passbook is a low-risk investment method that still yields high returns. Even if the market fluctuates, your money will continue to grow stably.

Benefits of choosing to open a savings account

- Build Sustainable Financial Habits: Saving is an excellent way to build long-term savings habits, helping you better control your personal finances, thereby creating a solid foundation for the future.

- Diverse Terms, Maximum Flexibility: You can choose a term that suits your plans. Short-term for easy withdrawal when needed, or long-term to optimize profits – you'll always have a flexible solution for every need.

- Convenient Management, Anytime, Anywhere: With the support of digital banking services like Internet Banking or Mobile Banking, tracking and managing your savings passbook becomes easy and fast, saving you time while keeping you informed about your financial situation.

4. Things to Know Before Opening a Savings Passbook

Before deciding to open a savings passbook, you should consider a few basic points:

4.1. Conditions for Opening a Savings Passbook

Before opening a savings passbook, customers need to meet certain basic conditions set by the bank. These typically include: being at least 18 years old, possessing valid identification documents (ID card or passport), and having full legal capacity to conduct financial transactions.

4.2. Minimum Deposit Amount to Open a Savings Passbook

Each bank has different minimum deposit requirements for opening a savings account. Typically, the minimum amount to open a savings passbook ranges from VND 500,000 to VND 1,000,000, catering to various customer segments.

The minimum amount required to open a savings account.

4.3. How to Calculate Savings Deposit Interest

Savings deposit interest is calculated based on the deposit amount, interest rate (%/year), and deposit term. Depending on the type of deposit, banks apply different calculation methods, most commonly for term and non-term deposits.

For term deposits, the interest rate is usually applied for the entire deposit term. The formula is:

|

Interest Earned = Deposit Amount x Annual Interest Rate (%) x Number of Deposit Days |

Meanwhile, for non-term deposits, the interest rate is typically lower and calculated based on the actual number of days the money is deposited:

|

Interest Earned = Deposit Amount x Daily Interest Rate (%) x Number of Deposit Days |

Note: Banks often calculate the number of days in a year as 360 days according to international standards. For long-term deposits, if the bank has an interest reinvestment policy, you can benefit from compound interest, meaning the interest earned is added to the principal to calculate interest for the next term.

Example:

Case 1: Term Deposit Suppose you deposit 100 million VND into a bank at an interest rate of 6% per annum for a 6-month term (180 days). Applying the formula:

Interest Earned=100,000,000 VND×6%×180/360=3,000,000 VND

Case 2: Non-Term Deposit You deposit 50 million VND at a non-term interest rate of 0.2% per annum for 15 days. Calculation:

Interest Earned=50,000,000 VND×0.2%×15/360=4,167 VND

Thus, after 15 days, the total amount you receive is 50,004,167 VND.

See also: The most accurate and commonly used method to calculate bank loan interest rates.

4.4. What are Maturity Date and Savings Passbook Settlement?

- Maturity Date: This is the last day of the deposit term, at which point you can withdraw the principal and interest or renew the savings for a new term.

- Savings Passbook Settlement: This is the process of closing a savings passbook, which includes withdrawing the principal and interest or rolling over to a new term if you choose to renew.

4.5. Can Customers Withdraw Savings Before Maturity?

Customers can withdraw money before maturity, but they will not receive the committed interest rate. Instead, a much lower non-term interest rate will apply. If possible, you should carefully consider before withdrawing early to avoid a loss of potential earnings.

Calculating interest for early withdrawal

4.6. Should You Open a Term or Non-Term Savings Passbook?

To decide whether to open a term or non-term savings passbook, you should consider your needs. Specifically:

-

Term Savings Passbook: Suitable for those who want to accumulate funds long-term with higher and stable interest rates. If you don't need access to the funds in the short term, this is a good option.

-

Non-Term Savings Passbook: Suitable for those who need flexibility and can withdraw money at any time. However, the interest rate will be lower compared to a term passbook.

5. Procedures for Opening a Savings Passbook at VPBank

To open a savings passbook at Vietnam Prosperity Joint Stock Commercial Bank (VPBank), you have two options: opening at a transaction counter or opening online. Here's a detailed guide for each method:

5.1. Procedures for Opening a Savings Passbook In-Branch

Step 1: Schedule an Appointment: Before visiting the branch, you should consider booking an appointment online to save time and ensure prompt service.

Step 2: Prepare Necessary Documents:

-

Identification: Valid ID card (CMND), Citizen ID (CCCD), or Passport.

-

Deposit Amount: Bring the amount of money you intend to deposit.

Step 3: Visit the Transaction Counter: At the counter, request assistance from a bank employee to open a savings passbook and follow their instructions.

Step 4: Receive Your Savings Passbook: After completing the procedures, you will receive your passbook. Please carefully check all information on the passbook to ensure accuracy.

5.2. Procedures for Opening Savings Online

Step 1: Register for Online Banking Services: If you don't already have a VPBank NEO account, you'll need to register by downloading the VPBank NEO app from the App Store or Google Play and following the instructions to create an account.

Step 2: Log in to the VPBank NEO App: Use your registered account information to log in.

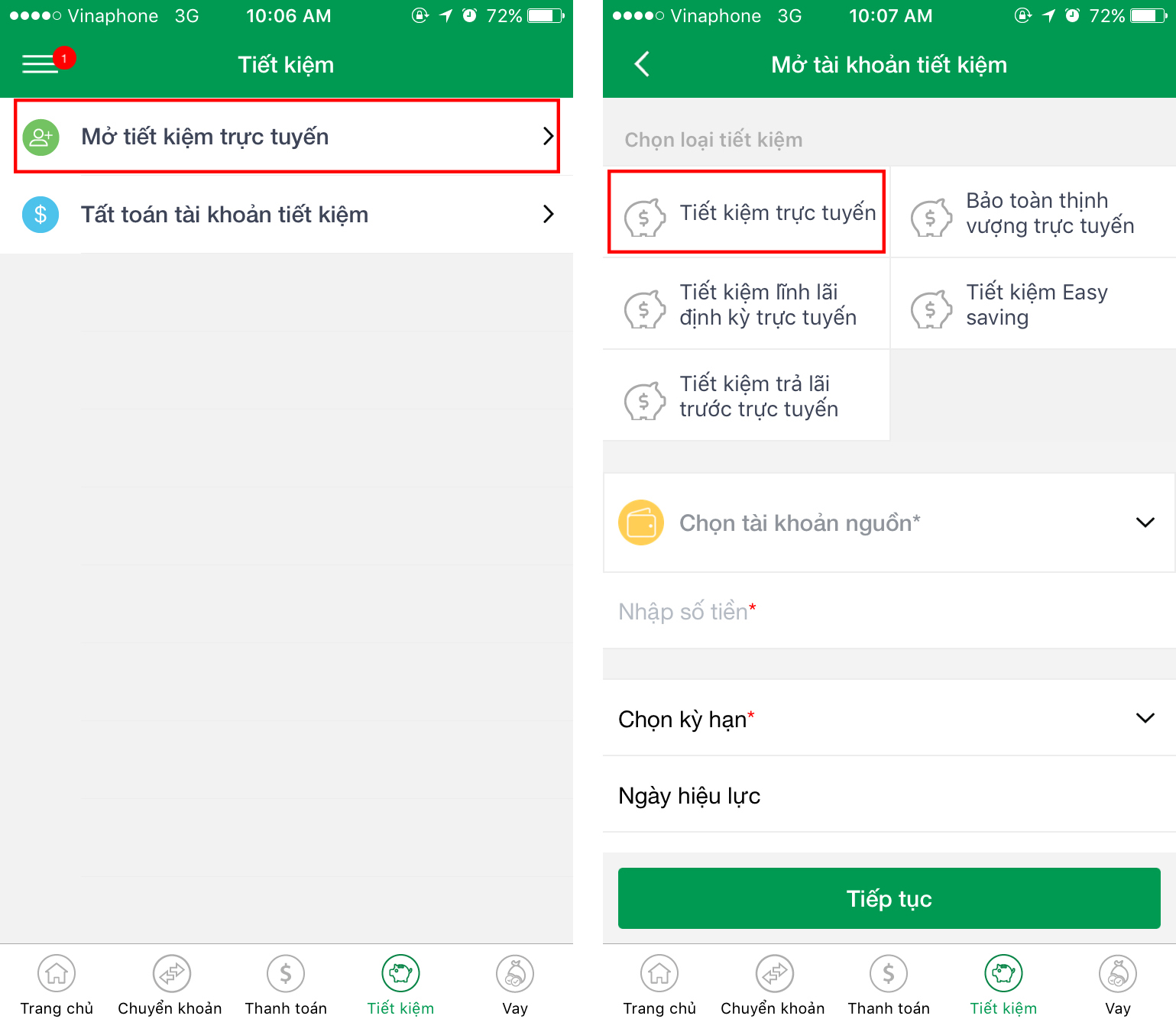

The interface for opening a savings account online via the bank’s app

Step 3: Open the Online Savings Passbook: From the main interface, you can open an online savings passbook by following these steps:

-

On the main screen, select the "Deposits" section.

-

Choose the type of deposit that suits your needs, e.g., Term Deposit, Easy Savings (installment term deposit), Phat Loc Thinh Vuong (Prosperity Development) Deposit, or Prime Savings (term deposit).

-

Enter the desired deposit amount, term, source account, and settlement method.

-

Carefully read the terms and conditions, then click "Continue."

-

Confirm the transaction: Enter the Smart OTP code to confirm and complete the online savings passbook opening.

Note: When opening an online savings passbook, you may be eligible for higher interest rates compared to opening in-branch.

You may be interested in:

- Can you withdraw from online savings accounts? Are there any penalties?

- What should you do with 100 million VND? 10+ hottest investment and business ideas

- What to do if you forget your Internet Banking password?

Thus, a savings passbook helps you accumulate your idle funds and provides peace of mind through its safety and stability. With simple opening conditions and diverse benefits, it's an optimal choice for anyone looking to manage their finances effectively.

So, why wait? Contact our hotline 1900.54.54.15 or visit www.vpbank.com.vn to open a savings passbook at VPBank and enjoy leading financial services today!

Chia sẻ:

![Lãi suất gửi tiết kiệm ngân hàng nào cao nhất? [05/2025]](/-/media/tin-tuc/2025/7fa2aaa9fbf041209316266b69dedbd7.png)