7 phương pháp quản lý chi tiêu cá nhân hiệu quả giúp tiết kiệm

Saving

26/04/2023

Currently, many people face financial challenges, including how to avoid overspending. Beyond increasing income, effective personal spending management is a key concern for those seeking greater financial abundance. To address these concerns, VPBank will share effective personal spending management tips in this article.

Mẹo quản lý chi tiêu cá nhân

1. What Is Personal Spending Management?

Personal spending management can be understood as effectively allocating your money into appropriate categories. This is a crucial step towards financial independence and freedom. By learning to manage your finances early, you can reduce financial stress.

Personal spending management involves creating your own financial plan, which includes tracking, reviewing, evaluating, and adjusting expenses based on real-time situations. This process can occur daily, monthly, or even annually.

Quản lý chi tiêu cá nhân là rất cần thiết trong xã hội hiện nay

Personal spending management encompasses:

-

The ability to plan expenditures.

-

The ability to plan savings.

-

Investment in necessary insurance.

-

Future investments and risk management.

Personal spending management directly impacts daily spending, income, and future investments. Therefore, if you understand this concept correctly, you will have better control over your cash flow. You can easily set future financial goals and be more proactive in resolving unexpected issues, minimizing unnecessary risks.

2. 7 Effective Personal Spending Management Methods

Here are 7 renowned and highly effective methods for personal spending management:

2.1. The "Pay Yourself First" Method

This method means saving first, then spending. Each month, or whenever you receive income, prioritize saving over spending on living expenses. By simply allocating about 10% of your monthly income to your savings, you have successfully implemented this method.

Afterward, you can confidently spend the remaining amount or divide it into multiple accounts for different purposes. This method is easy to implement and less time-consuming. However, its profit potential is not high, requiring patience.

Phương pháp “Pay Yourself First” là gì?

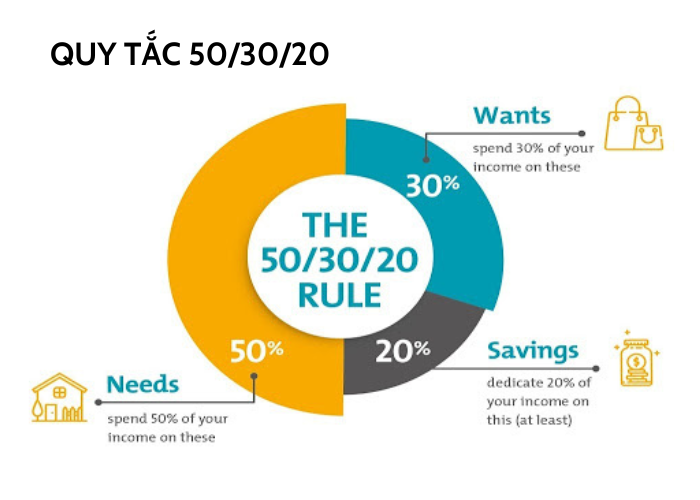

2.2. The 50/30/20 Method

This rule allocates 50% of your money to essential needs, 20% to savings and investments, and 30% to personal wants. This rule can be adjusted based on total income, living expenses, housing costs, or individual preferences, potentially leading to higher savings and investments. Additionally, for capital accumulation, investments should adhere to safety principles.

Phương pháp quản lý chi tiêu 50/30/20

The 50/30/20 rule is a classic principle of personal finance. Using this method, you will divide your income into three categories:

-

50% Basic and Mandatory Expenses: bill payments, electricity, water, food, rent, etc. (Can be determined from monthly bills, monthly transaction history, etc.)

-

30% Flexible Spending: shopping, entertainment, weddings, parties, etc., or other discretionary spending. (If possible, it's best to limit expenses in this category.)

-

20% Debt Repayment and Savings: Used for saving and paying off old debts. (This can help you cope with unexpected financial needs in life.)

Xem thêm: Lãi suất tiết kiệm ngân hàng nào cao nhất hiện nay?

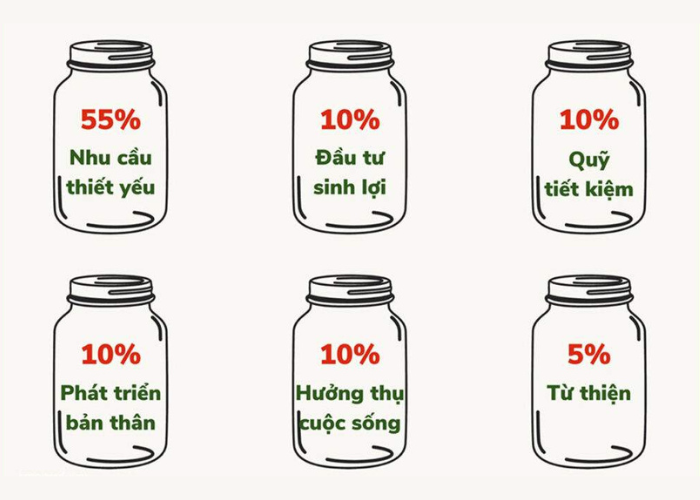

2.3. The 6 Jars Method:

To implement this method, you first need to divide your income into 6 different jars, each serving a specific purpose. The creator of this rule suggests that regardless of how much money you start with, divide it into these 6 financial jars.

6 chiếc lọ tài chính giúp quản lý chi tiêu dễ dàng hơn

Similar to the 50/30/20 method, the 6 jars financial rule is applied to divide income into different allocations:

- Jar 1 (55%): Necessary Expenses. These needs can include living expenses, rent, utilities, etc. Reconsider your spending if you allocate more than 55% of your total income to this jar.

- Jar 2 (10%): Long-Term Savings Fund. Long-term financial goals could be buying a house, a car, or starting a business. To manage this jar effectively, you can open a savings account or use a piggy bank.

- Jar 3 (10%): Education Fund. The money you put into this jar can be used for skill courses, seminars, etc., to enhance your knowledge. Knowledge will provide you with better career opportunities in the future.

- Jar 4 (10%): Personal Spending. In this jar, you can use the money for things that help you relax and feel comfortable, such as travel, shopping, self-care, etc.

- Jar 5 (5%): Long-Term Investment. You can use the money in this jar to invest in business, real estate, and other profitable investments to generate passive income. This money can help you cope with unemployment or unexpected financial risks.

- Jar 6 (5%): Charity. This portion is for charitable activities, helping others, etc. You can reduce this amount slightly, but it shouldn't be eliminated entirely, as sharing is essential in life.

2.4. The 10/20/70 Method

Derived from the three methods above, the advantage of this method is that it requires less intense spending oversight and offers greater flexibility. Essentially, you still divide your income into different categories and prioritize paying yourself first.

The allocations are as follows:

- 10% Emergency Fund: In this category, emergency funds take precedence over general savings.

- 20% Self-Development: Invest in knowledge, build quality relationships, etc.

- 70% Basic Expenses: Daily living, food, entertainment, bills, fuel, etc.

Xem thêm: Khái niệm tiết kiệm là gì? Tại sao ta cần phải sống tiết kiệm hơn?

2.5. The Envelope Saving Method

Saving money with envelopes means you allocate your income and place it into specific envelopes for particular purposes. Subsequently, you are only allowed to spend money within the confines of each envelope. This method helps you control your monthly expenses.

Recently, this method has become very popular on social media. To use this method, you need to prepare cash, envelopes, and follow these steps:

-

List the important expenses for the month and label each envelope accordingly.

-

Based on your estimated expenses, divide your cash and place it into each envelope.

-

For each purpose, you may only use the money from the corresponding envelope. Do not take money from other envelopes to replenish an empty one.

This is a way to cultivate patience. If implemented with discipline, this method can be highly effective for personal spending management.

2.6. Personal Spending Management Using the Kakeibo Journal:

Kakeibo, in Japanese, means "household finance ledger." It was created by journalist Hani Motoko in 1904. With this method, you can meticulously record your spending and saving activities using only a pen and notebook, rather than modern computer software.

Kakeibo is a ledger primarily designed to help Japanese homemakers manage and balance family expenses. Later, the Kakeibo ledger gained widespread use and became a favorite financial management method for many.

Phương pháp quản lý tài chính bằng sổ Kakeibo

The Japanese Kakeibo financial management method is also considered an excellent solution. You can use this journal by following these steps:

-

Record all monthly expenses that you are certain to incur (with specific amounts, if possible).

-

Calculate a specific amount to allocate for your savings and long-term financial goals. Ensure you are disciplined with that amount.

-

Divide your income into main categories (you can follow the principles mentioned above).

-

Based on the information about the money spent, commit to that amount. Adjust and cut unnecessary expenses.

-

In your monthly Kakeibo journal, carefully note any unsuitable purchases and adjust your plan accordingly.

This method helps the Japanese control their spending more easily to achieve other important life goals.

2.7. The 9-1 Financial Management Method of the Jewish People:

Simply put, the 9-1 rule states that expenses should not exceed 90% of your total income. If we persevere, not only can we escape poverty but also accumulate savings for ourselves. Therefore, "Never despise the money you save" is a universal lesson for wealth creation.

Có thể bạn quan tâm:

-

Đáo hạn sổ tiết kiệm là gì? Cách tính ngày đáo hạn chính xác

-

Cách tính lãi suất ngân hàng nhanh và phổ biến nhất hiện nay

The above article provides information related to effective personal spending management. We hope this article is helpful to you. Additionally, you can explore VPBank's fast online loan products with incredibly simple procedures, no collateral required, and loan limits up to VND 200 million. Don't forget to visit the VPBank website now to learn more about other attractive loan products

Share:

![Which Bank Offers the Highest Savings Interest Rates? [May 2025]](/-/media/tin-tuc/2025/7fa2aaa9fbf041209316266b69dedbd7.png)